Finding the right financial protection for your family shouldn’t involve weeks of waiting, multiple doctor appointments, or invasive blood tests. In 2026, the insurance landscape has shifted dramatically, making no-exam life insurance one of the most popular ways to secure a financial safety net.

Whether you are a busy professional, a young parent, or a senior looking for final expense coverage, understanding life insurance without a medical exam and blood test is crucial for making an informed decision. This guide explores how these policies work, the top-rated companies of 2026, and how to get same-day life insurance coverage from the comfort of your home.

What is No-Exam Life Insurance?

At its core, no-exam life insurance is a policy that allows you to apply for and receive coverage without undergoing a physical medical exam. Traditionally, life insurance required a “paramedical” visit where a professional would record your height, weight, and blood pressure, and collect blood and urine samples.

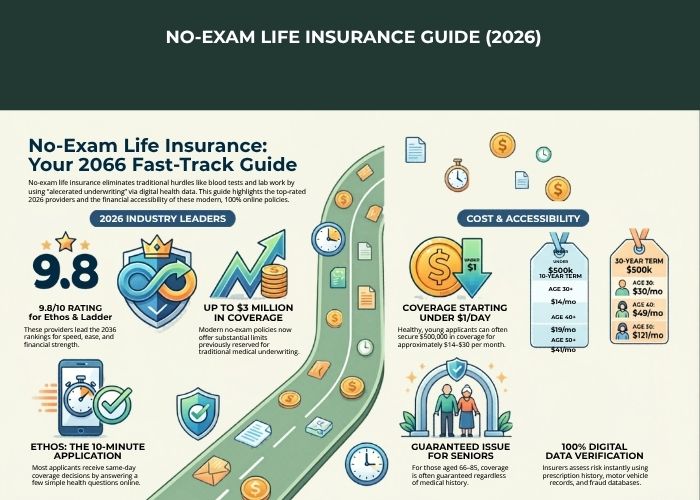

Today, modern “insurtech” companies use accelerated underwriting. Instead of physical lab work, they utilize sophisticated algorithms to analyze digital data, including your prescription history, motor vehicle records, and information from the Medical Information Bureau (MIB). This process turns what used to be a month-long ordeal into a digital experience that often takes less than 10 minutes.

Top 5 Best No-Exam Life Insurance Companies of 2026

Based on recent reviews for 2026, several companies stand out for their financial strength, ease of use, and competitive pricing.

1. Ethos Life: Best for Speed and Reliability

Ethos is widely considered the top choice for 2026 due to its 100% online application and high approval rates.

- Coverage Limits: Up to $3 million for term policies.

- Key Benefit: Most applicants receive same-day coverage and an instant decision.

- Added Value: Many policies include a free legal will and trust (worth up to $798).

2. Ladder: Best for Flexible Coverage

Ladder offers a unique “laddering” feature that allows you to adjust your coverage as your financial needs change.

- Coverage Limits: With up to $3 million available 100% digitally without an exam.

- Key Benefit: You can decrease your coverage (and your premiums) online with just a few clicks as you pay down your mortgage or as your children grow up.

- Financial Strength: Their carrier partners, such as Amica and Allianz, hold A+ (Superior) ratings from A.M. Best.

3. Fabric by Gerber Life: Best for Young Families

Fabric focuses on providing affordable, simple coverage for parents.

- Coverage Limits: Up to $5 million for term life.

- Key Benefit: Their application is designed for busy families and can be completed in about 10 minutes via their app or website.

4. SelectQuote: Best for Comparing Rates

If you want to see multiple options at once, SelectQuote allows you to compare over 70 different policies from highly rated carriers.

- Key Benefit: They claim users can save more than 50% by comparing the top-rated term life agencies.

5. SBLI (Savings Bank Mutual Life Insurance): Best for Legacy

SBLI has been protecting families since 1907 and offers stable, locked-in premiums.

- Key Benefit: Their policies include a digital lockbox for estate planning, helping you keep your financial documents organized for your beneficiaries.

Types of Life Insurance Without a Medical Exam

Not all no-exam policies are created equal. Depending on your health and age, you may qualify for different types of “no-needle” coverage.

1. Accelerated Underwriting (Term Life)

This is the most common option for healthy individuals aged 20 to 60. It provides high coverage amounts (often $1M to $3M+) at rates comparable to traditional policies.

- Best for: Income replacement, mortgage protection, and young families.

2. Simplified Issue Life Insurance

This type of policy is a “middle-ground” option. It requires you to answer a detailed health questionnaire but skips the physical exam.

- Best for: Applicants with minor, well-controlled health conditions who might not qualify for instant accelerated approval.

Next to Read : Money Management in Retirement – The essential guide

3. Guaranteed Issue Life Insurance

As the name suggests, you cannot be turned down for this policy regardless of your medical history, as long as you meet the age requirements (typically 50-85).

- Best for: Seniors or individuals with serious medical conditions looking to cover final expenses.

- Note: These policies have lower coverage limits (usually $5,000 to $50,000) and higher premiums per dollar of coverage.

How Much Does No-Exam Life Insurance Cost?

One of the biggest myths is that no-exam policies are always expensive. In reality, for healthy applicants, the cost is often identical to traditional policies.

Average Monthly Costs for a $500,000 No-Exam Term Policy (Healthy Applicants)

| Age | 10-Year Term | 20-Year Term | 30-Year Term |

| 30 | $14 | $20 | $30 |

| 40 | $19 | $29 | $49 |

| 50 | $41 | $66 | $121 |

(Data based on sample 2026 rates for healthy individuals)

Costs for Seniors (Guaranteed Issue)

For those looking for smaller “final expense” policies, the costs for a $10,000 policy typically range as follows:

- Age 60: ~$43 (Female) / ~$57 (Male) per month.

- Age 70: ~$64 (Female) / ~$87 (Male) per month.

Is No-Exam Life Insurance Right for You?

The Pros: Why People Choose No-Exam Coverage

- Speed: You can often go from “applying” to “fully covered” in the time it takes to drink a cup of coffee.

- Convenience: No need to schedule a nurse visit or fast for a blood draw.

- Privacy: The entire process is digital and can be done from home.

- Accessibility: It provides a path to coverage for those who have a fear of needles or very busy schedules.

The Cons: Potential Drawbacks

- Coverage Limits: If you need more than $3 million in coverage, you may still need to undergo a traditional exam.

- Health Requirements: To get the absolute lowest rates on a no-exam term policy, you generally need to be in excellent health.

- Potential for Exam: If your digital records show complex medical issues, the insurer may still request a physical exam to clarify your risk.

Common Myths vs. Reality

- Myth: You can only get a small policy without an exam.

- Reality: You can get up to $8 million in coverage through providers like Ladder, with significant portions available 100% digitally.

- Myth: “No-exam” means “no health questions.”

- Reality: Unless it is a guaranteed issue policy, you will still have to answer questions about your medical history, prescriptions, and lifestyle.

- Myth: There is always a waiting period for coverage to start.

- Reality: While guaranteed issue policies often have a 2-3 year “graded benefit” period, most no-exam term policies provide full coverage immediately upon approval.

How do insurers verify health data without a doctor visit?

Insurers verify your health and background data through a process called accelerated underwriting, which uses sophisticated algorithms and digital databases to assess risk in real-time without a physical exam.

The primary methods they use to verify your information include:

- Digital Prescription History: Insurers access pharmacy databases to review your past and current medications, which helps them identify potential chronic conditions or health risks you may not have fully disclosed.

- Motor Vehicle Reports (MVR): Your driving record is reviewed for high-risk behaviors, such as DUIs, reckless driving, or repeated serious violations, which insurers use to gauge overall lifestyle risk.

- The Medical Information Bureau (MIB): This industry-wide database allows insurers to check for inconsistencies in your past insurance applications, ensuring that the information you provide matches what you have told other carriers previously.

- Detailed Health Questionnaires: Applicants must complete a digital interview covering medical history, past surgeries, family health history, and tobacco use.

- Third-Party Data and Fraud Databases: Insurers utilize identity verification systems and other third-party reports to confirm your identity and look for signs of fraudulent activity.

- Digital Medical Records: While a doctor visit is not required, insurers may sometimes request existing records from your physician to verify a specific diagnosis or recent treatment if the digital data is unclear.

By processing this data through smart underwriting engines, companies can often provide an instant decision or same-day coverage to qualified applicants. However, if these digital checks reveal complex health issues or inconsistencies, the insurer may still require a traditional medical exam before final approval.

Step-by-Step: How to Apply for No-Exam Life Insurance

The process is designed to be user-friendly and efficient.

- Calculate Your Needs: Use an online calculator to determine if you need coverage for income replacement, mortgage protection, or just final expenses.

- Gather Your Info: Have your basic medical history, current medications, and social security number ready.

- Complete the Online Application: Answer questions honestly. Technology allows insurers to verify your data against third-party databases, so truthfulness is essential to ensure a claim is never denied later.

- Review Your Quote: Most platforms like Ethos or Ladder will give you a personalized price estimate in seconds.

- Activate Your Policy: Once approved, make your first payment. Your beneficiaries are now protected.

Your Estimated Life Insurance Need (DIME)

This is a simplified estimate. Review with a licensed financial professional.

Frequently Asked Questions (FAQs)

Can I get no-exam life insurance if I have a pre-existing condition?

Yes. Many applicants with mild or well-controlled conditions (like treated high blood pressure) can still qualify for accelerated term life. Those with more serious conditions may qualify for simplified issue or guaranteed issue policies.

Will no-exam life insurance cover a death from a pandemic or COVID-19?

Generally, yes. Life insurance policies typically do not exclude pandemics. However, you must be truthful about any current illnesses during the application process.

What is the “Free Look Period”?

Most top-rated companies like Ethos and Ladder offer a 30-day money-back guarantee (also known as a free look period). If you change your mind within the first month, you can cancel for a full refund of any premiums paid.

Can I convert a no-exam term policy to permanent coverage later?

Many policies include a conversion rider, allowing you to switch to a permanent whole-life policy later without a new medical exam, provided you do so within a specific timeframe.

Final Verdict: Should You Skip the Exam?

In 2026, no-exam life insurance is no longer a “niche” product for those in poor health. It has become the gold standard for healthy individuals who value their time and want a seamless digital experience.

If you are young, healthy, and need up to $3 million in coverage, skipping the needle is likely your best move. If you have complex health issues or need extremely high death benefits (over $5 million), you may still find better rates or higher limits through traditional underwriting.

About the Author: Sonal Macwan — Certified Financial Professional (CA), [License Number: 4421528] focused on retirement planning, life insurance basics, and long-term financial readiness for mid-career adults.

Education builds clarity. Personalized planning provides direction.

Protect your family’s future today. With the ability to get a quote in seconds and coverage in minutes, there’s no longer a reason to put off this essential piece of your financial plan.

💡 Your Money, Your Future — Get Expert Help Today

Making financial decisions about retirement, insurance, or estate planning can feel overwhelming. That’s why we’ve made it easier than ever to get professional guidance. With our simple Financial Solution Widget, you can connect instantly with a vetted financial.

Connect With An AdvisorThis content is provided for educational and informational purposes only and is not intended as financial, legal, tax, or investment advice.