Table of Content

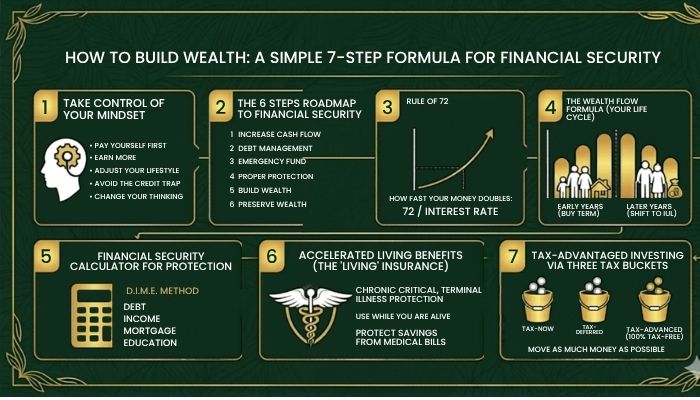

- Step 1: Take Control of Your Mindset

- Step 2: The 6 Steps to Financial Security Roadmap

- Step 3: The Algebra of Wealth and the Rule of 72

- Step 4: The Wealth Flow Formula (Your Life Cycle)

- Step 5: Using a Financial Security Calculator for Protection

- Step 6: Accelerated Living Benefits (The "Living" Insurance)

- Step 7: The Ultimate Wealth Strategy – Tax-Advantaged Investing via the Three Tax Buckets

- Final Thoughts: Don't Wait for the "Perfect" Time

Most people think building wealth is some big mystery. They think you need to be a math genius or have a huge inheritance to get ahead. But as a licensed financial professional, I’m here to tell you that’s just not true. After years of helping families, I’ve realized that financial success isn’t about luck; it’s about following a simple formula for financial security.

About the Author: Sonal Macwan — Certified Financial Professional (CA), [License Number: 4421528] focused on retirement planning, life insurance basics, and long-term financial readiness for mid-career adults.

Education builds clarity. Personalized planning provides direction.

In this post, we’re going to break down what I like to call the algebra of wealth. We’ll look at the exact steps you need to take to move from feeling stressed about bills to feeling confident about your future. If you’ve been looking for a financial security calculation that actually works for regular families, you’ve come to the right place.

Step 1: Take Control of Your Mindset

Before you can even think about a financial security calculator, you have to change how you look at money. Financial security is a behavioral shift. You can’t build a skyscraper on a swamp; you need a solid foundation.

According to the core pillars of money management, taking control involves five key moves:

- Pay Yourself First: You have to prioritize your family’s future before you pay everyone else.

- Earn More: Sometimes you just need a bigger shovel. Seeking a second income stream can speed up your success.

- Adjust Your Lifestyle: You need a budget that tells the difference between “wants” and “needs”.

- Avoid the Credit Trap: “Plastic money” is a dangerous game. If you can’t pay cash, you probably can’t afford it.

- Change Your Thinking: Successful people view money as a tool, not just something to spend.

Financial Need Analysis

Income Replacement & One-Time Needs

Existing Assets & Benefits

Retirement Income Gap

Emergency Fund Target

Step 2: The 6 Steps to Financial Security Roadmap

Once your mindset is right, it’s time to follow the technical sequence. This is the simple formula for financial security that moves you from being vulnerable to being protected.

- Increase Cash Flow: Manage your expenses and earn more to create the “fuel” for your plan.

- Debt Management: Consolidate and eliminate debt to free up your money.

- Emergency Fund: You need 3 to 6 months of income tucked away for surprises. This keeps you from falling back into debt when life happens.

- Proper Protection: You must protect your income and your assets from loss.

- Build Wealth: This is where you focus on outpacing inflation through active management.

- Preserve Wealth: The final step is about reducing taxes and making sure your money goes to your family, not the government or probate courts.

Is Ethos Wills and Trusts worth it? Read our 2026 Reviews about Ethos Trust and Will

Step 3: The Algebra of Wealth and the Rule of 72

Let’s talk about the math. Don’t worry, you don’t need a PhD. The most important part of your financial security calculation is something called the Rule of 72.

The Rule of 72 is a simple way to see how fast your money doubles. You just take the number 72 and divide it by your interest rate. For example, if you earn 6%, your money doubles every 12 years (72 / 6 = 12). If you earn 12%, it doubles every 6 years.

The sources are clear: “The person with the most doubles will win”. This is why the “high cost of waiting” is so dangerous. If you wait even a few years to start, you might lose one or two “doubles,” which could cost you hundreds of thousands of dollars in the long run.

Step 4: The Wealth Flow Formula (Your Life Cycle)

Your financial needs change as you get older. This is known as the Law of Decreasing Responsibility. This life cycle represents your wealth management strategy, moving from aggressive asset accumulation to capital preservation.

- The Early Years: When you are young, you usually have a mortgage, young kids, and high debt. You don’t have much wealth yet, so a loss of income would be a disaster. In this stage, the formula suggests “renting” wealth through Term Insurance because it gives you high coverage for a low cost.

- The Later Years: As you get older, the kids grow up and the mortgage gets paid off. Your risk shifts from “dying too soon” to “living too long” and paying too much in taxes. Now, you shift your focus to protecting wealth using Indexed Universal Life (IUL) Insurance, which can provide tax-free income for life.

The goal is to “Buy Term and Invest the Rest”. This ensures you have high protection when you are vulnerable and high tax-free growth when you are ready to retire.

Next to Read : Money Management in Retirement – The essential guide

Step 5: Using a Financial Security Calculator for Protection

How much insurance do you actually need? We use the D.I.M.E. method as a financial security calculator to figure that out.

- Debt: How much do you owe?

- Income: How many years of income does your family need to replace?

- Mortgage: How much is left on the house?

- Education: What will it cost to send the kids to college?

- By calculating these four areas, you get a clear picture of what it takes to protect your family’s lifestyle.

Your Estimated Life Insurance Need (DIME)

This is a simplified estimate. Review with a licensed financial professional.

Step 6: Accelerated Living Benefits (The “Living” Insurance)

Most people think life insurance only pays out when you die. But a modern simple formula for financial security includes Accelerated Living Benefits. These are benefits you can use while you are still alive if you are diagnosed with a chronic, critical, or terminal illness.

Next to Read : 2026 Wealth Building Strategy: Bridge the Retirement Gap

Why is this a big deal? Because a health crisis can “devastate” your retirement savings. Consider these facts:

- Medicare has limits: After 100 days, Medicare pays $0 for Long-Term Care.

- Nursing Homes are expensive: A private room can cost over $102,000 a year.

- Home Care isn’t cheap: Home health aides cost over $52,000 a year.

Living benefits provide a “liquidity source” that protects your savings from being eaten up by medical bills. Accelerated living benefits are a key part of modern life insurance policies, providing long-term care coverage and chronic illness protection while you are still alive.

Step 7: The Ultimate Wealth Strategy – Tax-Advantaged Investing via the Three Tax Buckets

If you want to preserve your wealth, you have to understand taxes. There are three “buckets” your money can sit in:

- Tax-Now: These are things like savings accounts or stocks where you pay taxes on the growth every single year.

- Tax-Deferred: This includes 401(k)s and traditional IRAs. You get a tax break today, but you pay taxes on everything—the principal and the growth—when you take it out. Warning: If you take out just $44,000 from these accounts, it can trigger taxes on up to 85% of your Social Security benefits.

- Tax-Advantaged: These are things like Roth IRAs and certain Life Insurance cash values. You use after-tax money to fund them, but the growth is 100% tax-free. They don’t trigger Social Security taxes, and they don’t have mandatory withdrawal rules (RMDs).

💰How to Build Tax-Free Retirement Income with IUL (2026 Guide)

The ultimate goal of the algebra of wealth is to move as much money as possible into the Tax-Advantaged bucket.

Explore Financial Planning Resources

Financial clarity improves when you have the right tools and explanations in one place. Explore our curated resources to better understand life insurance, retirement planning, and wealth-building strategies—designed to support informed, confident financial decisions.

Visit the Resources Page →Final Thoughts: Don’t Wait for the “Perfect” Time

It is important to understand “now is always the hardest time to invest”. There is always a war, an election, or an economic crisis that makes us want to wait. But the “high cost of waiting” is the biggest enemy of your financial security calculation.

Starting today—even with a small amount—is better than waiting years to try and “catch up”. Financial security isn’t about how much you make; it’s about the systems you put in place.

Are you ready to take control? Start by looking at the 7 steps and see where you are in your retirement planning journey. Build your defensive foundation first, then move up to offensive wealth building. Building a diversified investment portfolio today is the best gift for your future self.

This content is provided for educational and informational purposes only and is not intended as financial, legal, tax, or investment advice.