If you’re wondering how much Social Security money you’ll get in retirement, you’re not alone.

This is one of the most important numbers in your retirement plan—and thankfully, it’s easy to check.

About the Author: Sonal Macwan — Certified Financial Professional, focused on retirement planning, life insurance basics, and long-term financial readiness for mid-career adults. Content is educational, not legal or financial advice.

Education builds clarity. Personalized planning provides direction.

In this guide, I’ll show you exactly how to check your Social Security income online, what the numbers mean, and how to use them to make smarter retirement decisions.

No confusing terms. No guesswork. Just clear steps.

Before diving in, it helps to understand the full retirement picture. Our Retirement Planning Pillar breaks down Social Security, income strategies, timelines, and smart decisions so you can retire with confidence.

Why Checking Your Social Security Income Matters

Social Security is not meant to replace your full paycheck, but for many people, it becomes a steady monthly foundation in retirement.

How to maximize social security benefits and avoid taxes in retirement?

Knowing your estimated benefit helps you:

- Plan your retirement age

- Understand how much income you’ll need from savings

- Decide whether to retire early, on time, or later

- Avoid surprises later in life

Step 1: Go to the Official Social Security Website

Always use the official government site:

Never trust third-party websites that ask for your Social Security number.

Social security claiming strategies: how to maximize your benefits

Step 2: Sign In or Create Your Secure Account

When you click “Sign In,” you’ll see two options:

- Login.gov

- ID.me

Retirement Readiness Quiz for Working Women in California. Quick quiz.

Social Security no longer allows old usernames and passwords. You must use one of these secure systems.

What you’ll need:

- Email address

- Phone number

- Government ID (driver’s license or passport)

- A few minutes to verify your identity

Before deciding when to claim Social Security, you may want professional retirement income strategy consultation to avoid costly timing mistakes.

Once your account is set up, you won’t need to do it again.

Step 3: View Your Social Security Benefit Estimate

After signing in, you’ll see your personal Social Security dashboard.

This shows:

- Your estimated monthly benefit at age 62

- Your benefit at full retirement age (usually 67)

- Your benefit if you wait until age 70

These numbers are based on your work history and earnings so far.

How to Calculate Social Security and Reduce Taxes in Retirement (California Guide)

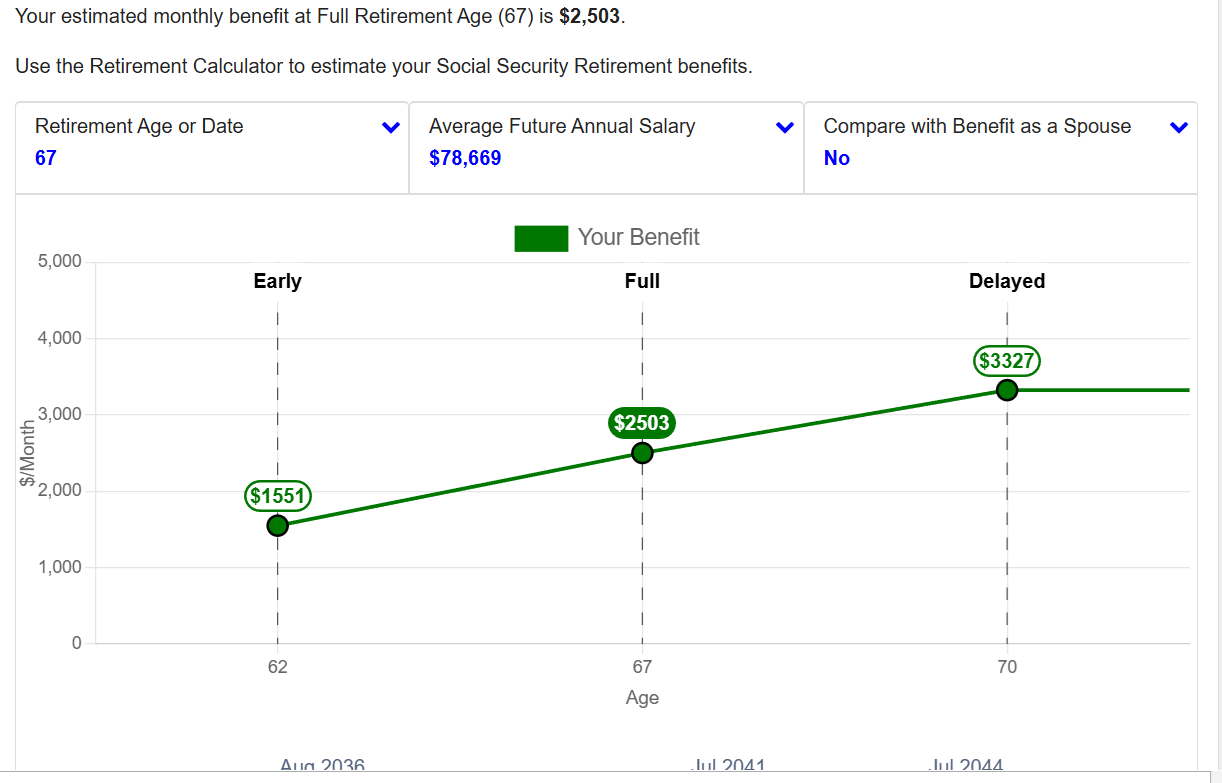

Step 4: Understand What the Numbers Mean

Example Graph Chart::

Example Graph Chart Explained in plain English::

This chart shows how much Social Security money you would get each month, depending on when you start taking it.

💼 401(k) Basics for Pre-Retirees: What You Need to Know Before You Retire

Three retirement choices:

1. Retire early (Age 62)

- Monthly benefit: $1,551

- You get money sooner, but much less every month for the rest of your life.

2. Full retirement age (Age 67)

- Monthly benefit: $2,503

- This is the standard amount Social Security plans for you.

- You get more per month than retiring early, without waiting longer.

3. Delay retirement (Age 70)

- Monthly benefit: $3,327

- You wait longer, but you get the highest monthly payment.

What the line means:

- The green line goes up because the longer you wait, the more money you get each month.

- The dots show the exact monthly amount at each age.

Key takeaway:

- Earlier = less money each month

- Later = more money each month

- Choosing when to retire is about balancing how soon you want income versus how much you want per month

This chart helps you see the trade-off clearly.

Here’s how to read your estimate:

Retire at 62 (Early)

- You get money sooner

- Monthly amount is permanently lower

Retire at Full Retirement Age (67)

- You receive 100% of your earned benefit

- Balanced option for many people

Retire at 70 (Delayed)

- Highest monthly payment

- About 8% more per year you wait after 67

💡 Waiting longer = more money per month

💡 Claiming earlier = smaller checks for life

Step 5: Check Your Earnings Record Carefully

Your benefit is based on your 35 highest-earning years.

Inside your account, you can:

- Review past earnings

- Spot missing or incorrect years

- Request corrections if needed

Even one missing year can lower your future income.

Explore Financial Planning Resources

Financial clarity improves when you have the right tools and explanations in one place. Explore our curated resources to better understand life insurance, retirement planning, and wealth-building strategies—designed to support informed, confident financial decisions.

Visit the Resources Page →Step 6: Use the Retirement Calculator Tools

The Social Security site includes calculators that let you:

- Change retirement ages

- Estimate future income

- Compare scenarios

This helps you answer questions like:

California Retirement Calculator

Your Projection (inflation-adjusted)

- Years to retirement: —

- Projected nest egg at retirement: —

- Income from portfolio (per month): —

- + Social Security (per month): —

- Estimated taxes (per month): —

- Estimated take-home (per month): —

What this assumes

- Contributions and returns compound monthly.

- Returns are converted to “real” (after inflation) for purchasing-power comparisons.

- SWR is applied to the inflation-adjusted nest egg.

- This is an educational estimate, not financial advice.

- “Can I afford to retire early?”

- “Is waiting worth it?”

- “How much income will I still need?”

Common Mistakes to Avoid

- ❌ Checking once and never reviewing again

- ❌ Assuming Social Security is enough by itself

- ❌ Claiming early without seeing long-term impact

- ❌ Not coordinating benefits with a spouse

Explore Financial Planning Resources

Financial clarity improves when you have the right tools and explanations in one place. Explore our curated resources to better understand life insurance, retirement planning, and wealth-building strategies—designed to support informed, confident financial decisions.

Visit the Resources Page →Social Security is a strategy, not just a number.

How This Fits Into Your Retirement Plan

Your Social Security income should work together with:

- Retirement savings (401(k), IRA)

- Pensions

- Investments

- Insurance and protection planning

When all pieces work together, retirement becomes less stressful and more predictable.

If you want to see how this topic fits into your bigger retirement strategy— including Social Security timing, income planning, and risk management— explore our complete Retirement Planning Guide.

Final Thoughts

Checking your Social Security income is one of the smartest financial moves you can make today—even if retirement feels far away.

It’s free.

It’s accurate.

And it gives you control over your future.

The earlier you understand your numbers, the more options you have later.

About MoneyMentor Hub

At MoneyMentor Hub, we focus on clear, real-world financial education—especially retirement and income planning. Our content is built to help everyday people make confident money decisions using trusted tools and official sources like SSA.gov.

Education builds clarity. Personalized planning provides direction. If you want to understand how these strategies apply to your financial goals, a thoughtful review can help you move forward with confidence.

Explore Your OptionsThis content is provided for educational and informational purposes only and is not intended as financial, legal, tax, or investment advice.