Complete Guide: How Life Insurance Works, Pays Out & Saves Your Family Financially

If you’ve ever wondered “how life insurance works in the US, especially in California” — you’re not alone. It’s one of the most misunderstood financial tools, yet one of the most powerful.

About the Author: Sonal Macwan — Certified Financial Professional, focused on retirement planning, life insurance basics, and long-term financial readiness for mid-career adults. Content is educational, not legal or financial advice.

Education builds clarity. Personalized planning provides direction.

Let’s break it down in a simple, real-world way so you can actually use life insurance strategically—not just buy it blindly.

🧠 What Is Life Insurance (In Plain English)?

Life insurance is a financial safety net.

You pay a monthly or yearly premium to an insurance company. In return, they promise to pay a tax-free lump sum (called a death benefit) to your chosen beneficiaries when you pass away.

Think of it as:

👉 “Income replacement + financial protection for your family”

🧩 What Most People Don’t Tell You About Life Insurance (Insider Insights)

There are many myths and misconceptions about life insurance. As a general thought, life insurance are believed to be paid only when someone is dead. But all these misconceptions can be wrong. It is better to know how life insurance works, from industry standards.

Based on industry insights from established insurers like North American Company, life insurance is not just a payout tool—it’s a multi-functional financial asset.

💡 1. Life Insurance Can Work While You’re Still Alive

Many people think life insurance only pays after death—but that’s outdated thinking.

👉 Modern policies (especially permanent ones) can provide:

- Access to cash value for emergencies

- Ability to borrow or withdraw funds

- Option to accelerate death benefits if diagnosed with chronic or terminal illness

✔ This is often called “living benefits”—and it’s a major shift in how policies are used today.

💰 2. Your Premiums Can Be “Leveraged” Into Larger Wealth

Here’s a powerful concept:

👉 A relatively small premium can instantly create a much larger financial benefit

Example:

- You pay $1,500/year

- Your family gets $250,000 coverage immediately

This is called financial leverage, and it’s one of the biggest advantages of life insurance.

📈 3. Permanent Life Insurance Builds Tax-Deferred Wealth

Unlike term policies, permanent life insurance can:

- Grow cash value over time

- Earn interest (sometimes tied to market indexes)

- Accumulate funds tax-deferred

👉 This makes it comparable (in some ways) to:

- Savings accounts

- CDs

- Money market funds

…but with added tax advantages and protection.

🏦 4. Life Insurance Can Replace Low-Performing Investments

Some strategies involve repositioning money from:

- CDs

- Savings accounts

- Low-yield investments

👉 Into life insurance for:

- Better long-term growth potential

- Tax advantages

- Legacy planning benefits

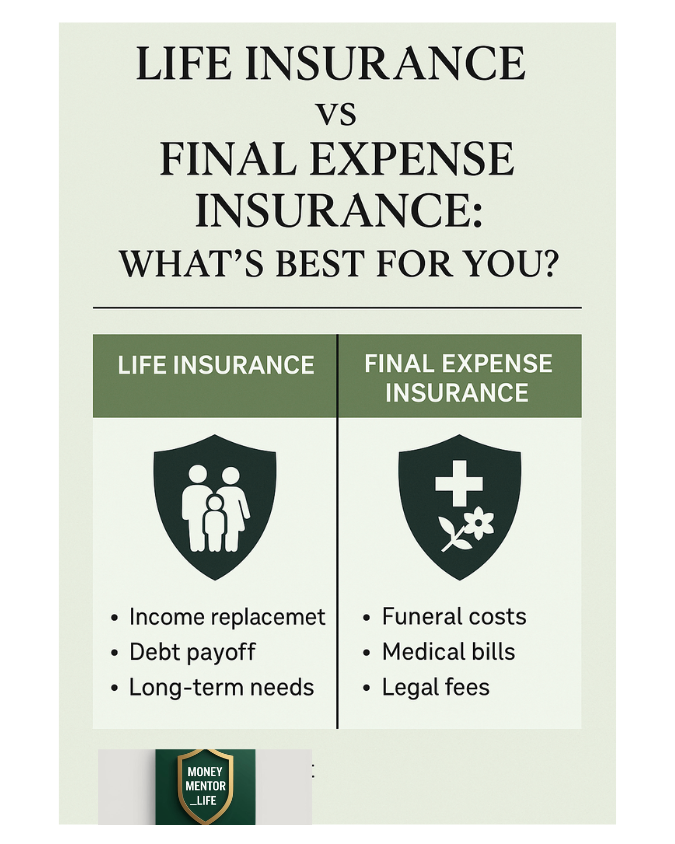

👨👩👧 5. It’s Designed to Replace Income (Not Just Cover Funeral Costs)

A key use case often overlooked:

Life insurance is meant to replace income and maintain lifestyle.

Example:

- Cover mortgage

- Fund kids’ education

- Replace lost salary

Insurance professionals often calculate coverage based on:

- Income replacement until retirement

- Household contributions (even unpaid work)

Your Estimated Life Insurance Need (DIME)

This is a simplified estimate. Review with a licensed financial professional.

⚖️ 6. There Are Trade-Offs You Should Know

Although life insurance is fundamental for a secure financial planning, here are real considerations:

- Policy fees and insurance charges

- Possible surrender charges

- Need for consistent funding

- Potential tax implications (e.g., MEC rules)

👉 Translation: Life insurance is powerful—but only when structured correctly. Therefore, it helps to consult a licensed financial professional to make your financial planning future proof.

🔄 7. You Can Combine Policies for Smarter Coverage

Many experts recommend a hybrid approach:

- Term insurance → cheap, high coverage (short-term needs)

- Permanent insurance → wealth building + long-term strategy

👉 This gives you both affordability and flexibility.

🧠 Why This Matters for You

By understanding these advanced features, you move from:

❌ Buying insurance blindly ➡✅ Using life insurance as a financial strategy tool️

🔍 How Life Insurance Policies Work (Step-by-Step)

Here’s exactly how life insurance policies work:

1. You Apply

- Provide health, income, and lifestyle details

- May require a medical exam

2. You Choose Coverage

- Example: $500,000 or $1,000,000 policy

3. You Pay Premiums

- Monthly or annually

4. Policy Stays Active

- As long as you keep paying

5. Beneficiaries Get Paid

- When you pass, insurer pays out the death benefit

Financial Terms Every one Should Know – Glossary of Financial Terms in Simple English

💰 How Life Insurance Pays Out (What Actually Happens)

This is one of the most confusing yet important questions: “how life insurance pays out”

Here’s the real process:

- Beneficiary files a claim

- Provides death certificate

- Insurance company verifies claim

- Payout is issued (usually within 14–60 days)

💡 Payout Options:

- Lump sum (most common)

- Installments

- Trust-managed payouts

👉 Most claims are approved quickly if the policy is active and honest disclosures were made.

How Life Insurance Works in the US (Especially California)

If you’re in California, here’s what matters:

✔ Regulated by:

✔ Consumer Protections:

- “Free look” period (usually 10–30 days)

- Strict disclosure rules

✔ Community Property Laws:

- Spouses may have legal claim depending on policy setup

✔ Key Tip:

Always clearly define primary and contingent beneficiaries to avoid legal complications.

💸 How Life Insurance Is Taxed (Important!)

Another big question: “how life insurance is taxed” . But these questions are answered in depth from resources like IRS websites.

✅ The Good News:

- Death benefits are generally 100% tax-free (federal)

⚠️ Exceptions:

- Interest earned on payouts → taxable

- Estate tax may apply for very large policies

- Cash value withdrawals (in some policies) may be taxed

🔄 Types of Life Insurance (Quick Breakdown)

🟢 Term Life Insurance

- Cheapest option

- Covers 10, 20, or 30 years

- Best for income protection

🔵 Whole Life Insurance

- Lifetime coverage

- Builds cash value

- Higher premiums

🟡 Universal Life Insurance

- Flexible premiums

- Investment component

🆚 How to Compare Life Insurance Quotes Online (Smart Way)

If you’re searching “how can I compare life insurance quotes online”, here’s the strategy:

Step 1: Compare Apples to Apples

- Same coverage amount

- Same term length

Step 2: Check Financial Strength

- Look for A-rated insurers (AM Best ratings)

Step 3: Evaluate Cost vs Value

- Cheapest isn’t always best

Step 4: Use Online Comparison Tools

- Aggregators save time

- Get multiple quotes instantly

Step 5: Look for:

- Riders (critical illness, disability)

- Conversion options

- Customer reviews

⚠️ Common Mistakes to Avoid

- ❌ Waiting too long (rates increase with age)

- ❌ Underinsuring

- ❌ Not updating beneficiaries

- ❌ Choosing based only on price

🧾 Final Thoughts

Life insurance isn’t just about death—it’s about financial security, legacy, and peace of mind.

If structured properly, it can:

- Replace income

- Cover debts

- Fund education

- Build generational wealth

FAQ

❓ How life insurance pays out in real life?

Most policies pay within 14–60 days after claim approval, often as a tax-free lump sum.

❓ How life insurance policies work long-term?

They can evolve from simple protection into cash-generating financial assets (depending on type).

❓ How life insurance is taxed in California?

Generally tax-free for beneficiaries, but estate and investment-related taxes may apply.

❓ How life insurance works in US vs California?

California adds consumer protections and legal considerations (like community property rules).

❓ How can I compare life insurance quotes online effectively?

Use comparison tools, match policy terms, and evaluate insurer ratings—not just price.

This content is provided for educational and informational purposes only and is not intended as financial, legal, tax, or investment advice.